If you’re hiring an AEO consultant for fintech compliance, the right partner is the one that can earn AI citations without creating review headaches. This is a shortlist article, not a concept explainer. Below, you’ll get seven vendors mapped to specific needs: Insivia for best overall fit, Croton Content for compliance-heavy content, iPullRank for technical AEO execution, First Page Sage for authority building, The ABM Agency for full-funnel growth, Omnius for enterprise or multi-region scale, and Notebook Agency for a boutique budget option. Each profile carries the decision data you came for, plus one honest tradeoff, so you can build a shortlist in a few minutes and skip the ones that don’t fit regulated finance.

Why Fintech Brands Need a Compliance-Aware AEO Consultant

AI answer engines compress choice. When a buyer asks ChatGPT or Perplexity for the best payments platform or lending API, the engine names a handful of options instead of a page of blue links. That shift changes the job. You now need a vendor who can shape what gets cited, not just what ranks.

Compliance changes the job again. Finance claims, required disclosures, and legal approvals break generic answer engine optimization playbooks that assume you can publish fast and iterate later. A regulated brand cannot ship a bold comparison page overnight. Every claim runs through review first.

There’s also the trust risk. Finance sits squarely in the “your money or your life” category, where AI engines weigh source credibility hard. Vague, unsupported, or overpromotional content can damage how your brand shows up in an answer, or keep you out of it entirely. Agencies that know SEO but not regulated-review workflows often create content that legal has to rewrite, which wastes weeks and burns goodwill with your compliance team.

So the commercial decision is narrow. You want a vendor who can balance three things at once: visibility in AI answers, compliance discipline, and reasonable speed. Get that balance right and you win better AI citations, safer messaging, and more qualified demand from regulated audiences. Miss it and you get either invisible content or a compliance mess. If you want the broader context first, our overview of compliance-aware citations for fintech covers the category-level thinking behind these picks.

How We Evaluated These AEO Consultants and Agencies

We scored each vendor against six criteria that matter specifically for regulated finance, not generic marketing. The best vendors in this category tend to win on process maturity, not a strong sales deck.

- Fintech compliance expertise: proof they understand regulated claims, disclosures, and review cycles.

- AEO and GEO methodology: a real process for AI visibility, not a rebranded SEO offer.

- Proof of results: case studies, citations, AI visibility evidence, or named financial clients.

- Technical depth: structured data, entity clarity, crawlability, and information architecture.

- Content strategy: the ability to build compliant authority content, not just publish generic posts.

- Fit for regulated teams: whether they can coordinate with legal, product, and brand stakeholders.

The disqualifiers are just as important. No fintech examples, no review workflow, and no technical detail all push a vendor down the list. A firm that cannot explain how it handles legal approval is a risk, no matter how sharp its pitch sounds. For a deeper look at the tradeoffs behind these criteria, our guide on choosing between an AI visibility agency and a tool is a useful companion read.

7 Best AEO Consultants for Fintech Compliance

Here are the seven consultants and agencies worth shortlisting, ranked and labeled by the buyer they fit best. Every profile follows the same shape: what it is, why it matters for regulated finance, the key benefit, and one honest tradeoff. In regulated fintech, the best vendor is usually the one that can show how it manages approvals, structured content, and AI citations together.

1. Insivia: Best Overall Fit

Insivia is a fintech-focused AEO and GEO agency for regulated brands that want answer-engine visibility and compliance-aware messaging in one program. It fits teams that need trust and citations together, not just traffic. The firm runs a formal AEO and GEO methodology backed by an AI Engine Auditing platform that checks visibility across ChatGPT, Perplexity, Gemini, and Claude, which gives you a real baseline instead of a guess. That auditing layer matters in finance, because knowing which engines already misread your brand tells you where the review-heavy content work should start. The honest limitation: this is built for strategic buyers who want a structured program, so a team that only needs a one-off fix will find it heavier than necessary.

- Best for: Regulated fintech brands wanting AEO, GEO, and compliance-aware messaging in one program

- Pricing model: Custom engagement

- Standout feature: Formal AEO and GEO methodology plus an AI Engine Auditing platform across major answer engines

2. Croton Content: Best for Compliance-Heavy Content

Croton Content is a video-first AEO, SEO, and GEO agency that works exclusively with financial brands, using compliance-cleared content to earn AI citations. It’s the strongest pick for teams whose bottleneck is regulated content itself: disclosures, approved claims, and legal sign-off. The differentiator is a YouTube-first model that turns one approved asset into several discovery surfaces at once, including YouTube ranking, Google video placement, and LLM citations. When AI engines summarize finance answers, having one compliance-cleared source powering multiple surfaces beats maintaining separate approvals for each channel. The tradeoff is real: this shines when video-led content is acceptable, and it’s a weaker match if you want a strictly text-based program.

- Best for: Financial brands that want AI citations as an outcome of a compliant content workflow

- Standout feature: Compliance-cleared video that creates three discovery surfaces from one approved asset

3. iPullRank: Best for Technical AEO and GEO Execution

iPullRank is an enterprise SEO and content strategy firm built for structured data, entity clarity, site architecture, and AI crawlability. It fits fintech products with complex taxonomies, legacy pages, and sprawling catalogs that answer engines struggle to interpret cleanly. The strength here is relevance engineering: deep work on how AI systems retrieve, structure, and select sources. That precision matters because messy architecture can block a model from understanding your products and how they relate, no matter how good the copy is. Our primer on building an AEO content structure shows why that groundwork comes first. The tradeoff: iPullRank is technical-first, so if your main gap is heavy editorial production, you’ll want to pair it with a content team.

- Best for: Fintech platforms with complex taxonomies needing clean AI interpretation

- Standout feature: Relevance engineering and deep technical understanding of AI retrieval

4. First Page Sage: Best for Authority Building

First Page Sage is a written SEO and AEO agency focused on fintech and financial services, built around subject-matter content and expert-driven publishing. It fits brands that need to become the trusted voice in a category rather than just chase rankings. The core strength is long-form thought leadership and educational content that establishes real authority. That matters in finance, because AI citations tend to favor credible, well-structured sources over thin promotional pages. The candid limitation: authority building is slower than a technical fix, and the firm carries a higher minimum engagement, so this suits buyers who can invest for the medium term rather than chase a quick win.

- Best for: Fintech brands building topical authority and category trust

- Pricing model: Minimum engagement around $10,000 per month

- Standout feature: Expert-led thought leadership content for YMYL credibility

5. The ABM Agency: Best for Full-Funnel Growth Support

The ABM Agency ties AEO to target accounts, pipeline, and revenue for fintech teams selling high-value deals to buying committees. It fits brands that need AI visibility to reach the right accounts, not just generate broad traffic. The standout is an account-based approach to GEO, where content is optimized around the specific questions each committee member asks during vendor research. That framing matters because visibility only pays off when it lands in front of accounts you can actually close. The tradeoff: this can be overbuilt for a smaller team that only needs a narrow AEO program, since the full account-based system carries more moving parts.

- Best for: Enterprise and mid-market fintechs needing AI visibility tied to pipeline

- Standout feature: Account-based GEO built around buying-committee questions

- Free audit or trial: Complimentary AI optimization audit offered

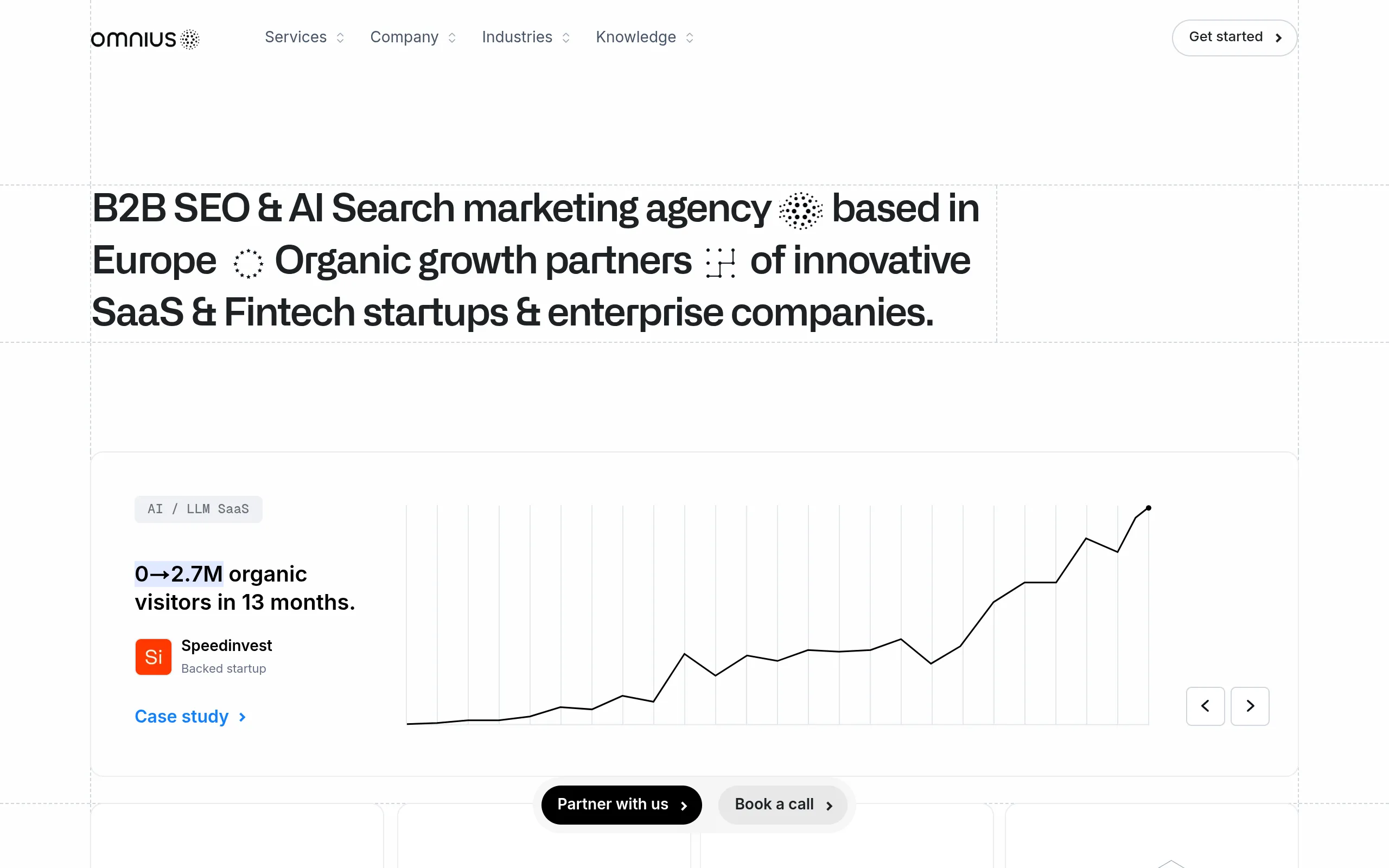

6. Omnius: Best for Enterprise or Multi-Region Fintech

Omnius is a B2B SEO and GEO agency for SaaS and fintech companies, strong on programmatic SEO and AI-first visibility at scale. It fits larger fintech teams, global audiences, and organizations with layered governance across markets. The value shows up in complex, multi-region execution, where localization, compliance variation, and cross-team coordination pile up fast. A programmatic, data-driven content approach helps you scale across regions without losing structure or consistency. The tradeoff: this works best when you already have clear internal ownership, because a larger program needs someone on your side to steer approvals and priorities. If you’re weighing scale, our breakdown of picking an enterprise GEO agency covers the governance questions to raise early.

- Best for: Multi-region and enterprise fintech teams scaling AI visibility

- Standout feature: Programmatic, data-driven content built for scale

7. Notebook Agency: Best Boutique Option

Notebook Agency is a boutique AEO and SEO firm with a proprietary trust-alignment framework and live citation monitoring. It fits teams that want hands-on attention and focused AEO support without enterprise overhead or layers of account management. The standout is the pairing of a documented methodology with named financial credentials and monitoring that tracks citations as they change. That combination gives smaller teams both credibility and a feedback loop, which is hard to find at boutique scale. The honest tradeoff: a compact team means narrower capacity and less breadth than a full-service agency, so if you need content production, technical work, and digital PR all at once, this may stretch thin.

- Best for: Smaller fintech teams wanting focused, monitored AEO support

- Standout feature: Trust-alignment framework plus live citation monitoring

Quick Comparison Table

Use this table to shortlist in under a minute. The fastest buying decisions in fintech usually come down to fit, governance, and execution model, not raw capability. The order mirrors the ranked list above.

| Consultant | Best for | Compliance strength | Technical depth | Ideal stage |

|---|---|---|---|---|

| Insivia | Overall fit | High | High | Growth to enterprise |

| Croton Content | Compliance-heavy content | Very high | Medium | Growth |

| iPullRank | Technical execution | Medium | Very high | Enterprise |

| First Page Sage | Authority building | High | Medium | Growth to enterprise |

| The ABM Agency | Full-funnel growth | Medium | Medium | Mid-market to enterprise |

| Omnius | Enterprise, multi-region | Medium | High | Enterprise |

| Notebook Agency | Boutique budget | High | Medium | Startup to growth |

We picked these seven by scoring each against fintech compliance expertise, AEO and GEO methodology, proof of results, technical depth, content strategy, and fit for regulated teams. Vendors with no fintech examples, no review workflow, or no technical detail were ranked lower. The list reflects genuine merit and the providers surfacing across current fintech AEO research, not a padded round number.

What to Ask Before You Hire

Run every shortlisted vendor through these questions. The right partner should explain workflow, not just tactics, because compliance bottlenecks are part of the job, not an afterthought.

- Show me two fintech case studies and the exact deliverables you shipped.

- How do you handle legal review, disclosure language, and regulated claims before publishing?

- Which technical fixes would you prioritize first, especially schema, entity cleanup, and internal linking?

- How do you measure AI citations, brand mentions, and qualified leads from answer engines?

- What do the first 90 days look like, including audits, content, approvals, and reporting cadence?

- What will you not do, so I can see your risk awareness rather than an overpromise?

Weight the answers by how specific they are. A vendor who describes a real approval loop, names the technical fixes it would tackle first, and admits what it won’t touch is telling you it has done this in a regulated setting. Vague reassurance signals the opposite. If you want to sharpen these questions further, our guide to hiring a generative engine optimization consultant covers the deeper vetting steps.

FAQs

What should I look for in an AEO consultant for fintech compliance?

Look for a vendor that pairs answer-engine visibility with a real compliance review workflow. The strongest picks show fintech case studies, a documented AEO or GEO process, and clear coordination with legal and product teams. Ask specifically how they handle disclosures and regulated claims before publishing, since that is where generic agencies fall down.

How is AEO different from SEO for fintech companies?

SEO aims to rank your pages in a list of blue links, while AEO aims to get your brand named and cited inside an AI-generated answer. For fintech, that difference is sharp: an answer engine may summarize your product in one sentence, so the accuracy and structure of your source content matters more than raw keyword placement. Both still work together, but AEO governs how you show up in ChatGPT, Perplexity, and AI Overviews.

Can an agency optimize for AI answers without creating compliance risk?

Yes, when the agency builds compliance into the workflow rather than bolting it on. The right partner drafts claims that survive legal review, handles required disclosures inside the content structure, and routes assets through approval before they ship. Picture a lending brand that needs every rate claim substantiated: a compliance-aware vendor writes the content so the disclosure and the citation-worthy answer live in the same approved page, so nothing gets rewritten after the fact.

How long does it take to see AEO or GEO results in fintech?

Expect a few months, not weeks, especially in regulated finance where approvals slow the publishing cycle. Technical fixes like schema and entity cleanup can register faster, while authority-driven citation gains build over a longer runway of 3 to 6 months. The review layer adds time, so budget for it up front.

Do I need technical SEO, content strategy, or digital PR for AEO?

Most fintech programs need all three, but the priority depends on your gap. If answer engines misread your products, start with technical work on structure and entities. If you’re invisible in your category, lead with authority content and earned media that build the trust signals AI engines favor in finance.

Matching the Right Consultant to Your Need

The most common hiring mistake is choosing a vendor for AEO buzzwords instead of compliance fit and proof. Map your need to the right type first. Compliance-first buyers should start with the vendors strongest on regulated content and workflow discipline, like Croton Content or Insivia. Technical-first buyers should favor a firm that can clean up structure, entities, and crawlability, which points to iPullRank.

Authority-first buyers should pick the strongest thought-leadership option and accept a longer runway. Full-service buyers who need AEO tied to pipeline should look at an account-based growth partner. Enterprise or multi-region teams should weigh governance, scale, and coordination depth, while boutique buyers accept narrower scope in exchange for hands-on attention and speed.

Whichever direction you lean, request an audit, ask for sample deliverables, and demand fintech-specific proof before you sign. Want to see where you stand first? Request a fintech AEO audit and compare compliance workflows before you hire.